On the S-Spot:

The celebrated point of equilibrium, the break-even point

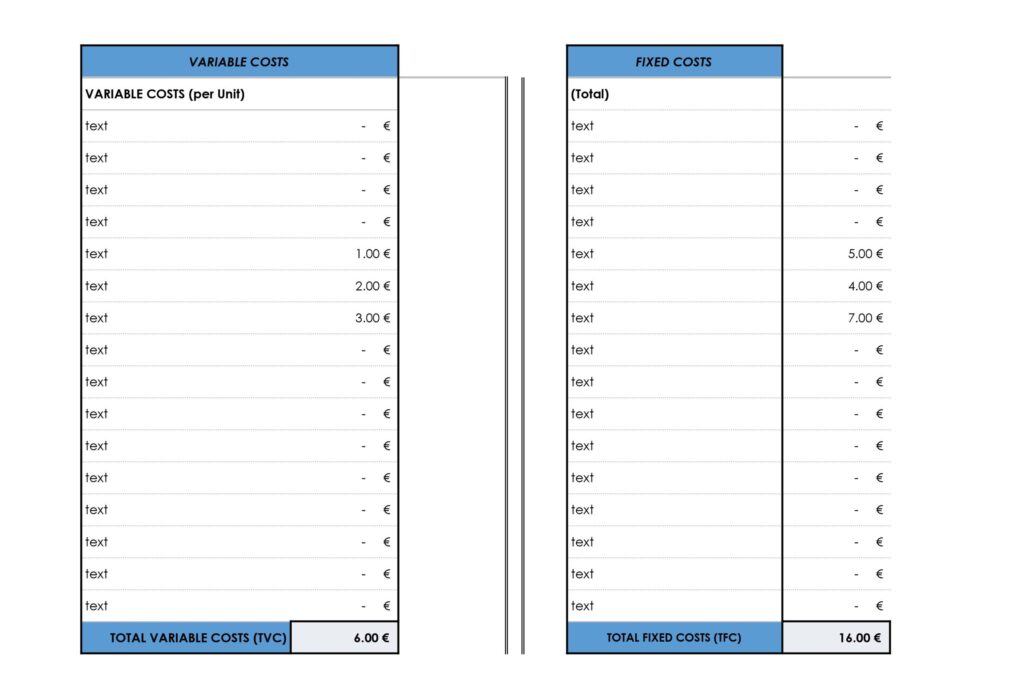

The break-even point is a fundamental concept in economics, representing the point at which

a business's revenue equals its costs.

An understanding of the breakeven point enables the evaluation of the influence of

alterations in activity volume, product price, fixed costs, and variable unit costs on the

profitability of the exploitation. The advantage of the break-even point is that it can be applied

in all business contexts and across all industry sectors, regardless of size.

The break-even point is a significant tool in many areas of business, including the launch of a

new venture, the introduction of new products, a change of business model, a price analysis,

and the decision to outsource. It is important to note that the break-even point is variable in

time and is influenced by changes in variable unit costs, fixed expenses, and selling prices.

Profitability is the primary objective of any business owner. However, before management

can generate a profit, they must first achieve a state of equilibrium, or break even.

Consequently, a break-even analysis should be regarded as a fundamental tool that can

provide a snapshot of a business's position at a specific point in time. This analysis should be

employed in conjunction with other financial measures to gain a comprehensive

understanding of the business's financial status.

By Professor López